Even with a great idea in mind, starting a business is tough. It may require resources, knowledge, capital, and even a permit or license – and existing competitors won’t make your life any easier. Entrepreneurship is an exciting adventure, and we are all attracted by potential profit. But aspiring entrepreneurs must consider how tough the barriers to entry are to see if entering a market is technically possible.

Even when it is technically possible, entering a new market does not guarantee success. That is why I like to differentiate the two types of barriers to entry: those that prevent access to a market and those that prevent new entrants from having a fighting chance at making a profit.

I apologize if you’re an aspiring entrepreneur and this article’s introduction sounds a bit depressing. But keep in mind that once established, businesses benefit from being in a market that is difficult to enter. As I said above, new entrants are attracted by the potential for profits and can be stopped by barriers to entry.

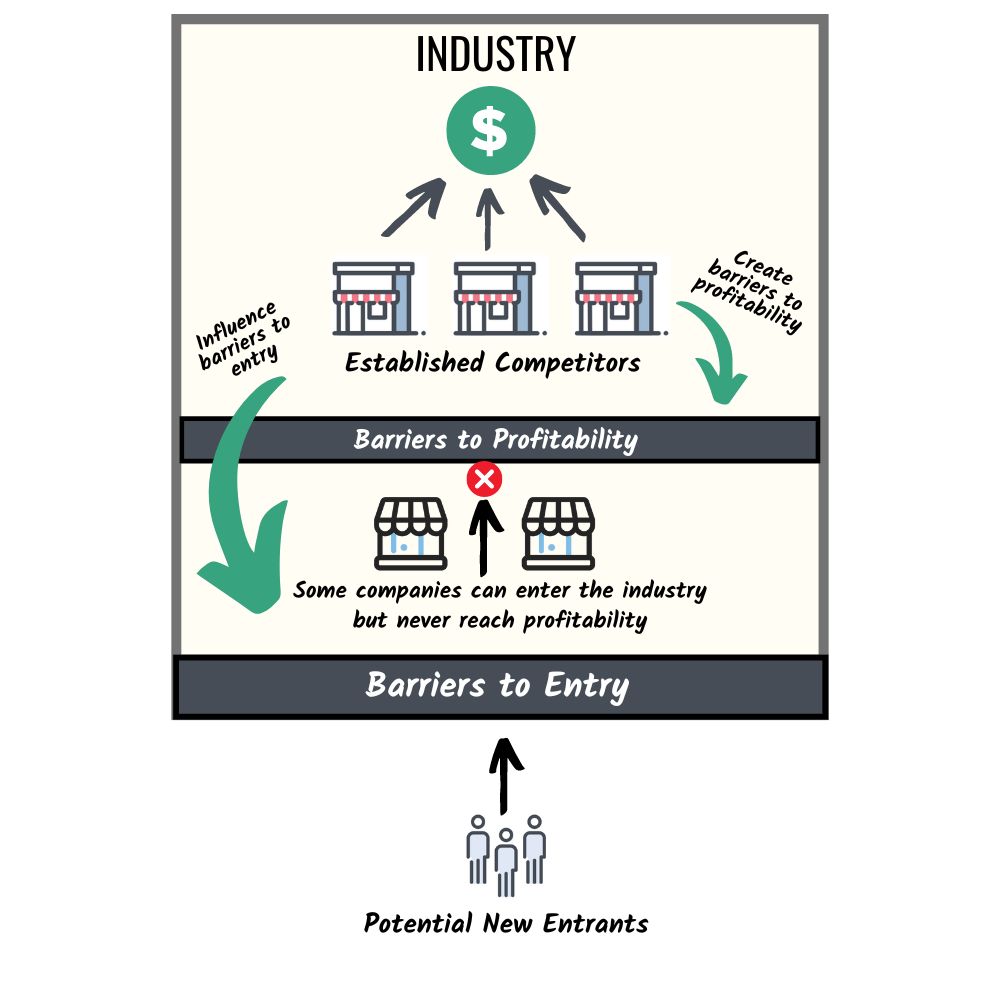

Barriers to entry can make it difficult, or even impossible, for a new competitor to operate in a market. There are many ways to categorize these barriers to entry, but I like to classify them into what I call barriers to entry and and barriers to profitability. Barriers to entry are what make it possible or not for a new competitor to enter the market, while barriers to profitability are what impact its chances to operate efficiently and ultimately to generate a profit.

Barriers to Entry

Government regulations are a good example of barriers to entry. Cable companies are heavily regulated due to their infrastructure, presence on public land, and their need for a license to operate. Without this license, you can’t start your own cable company, no matter how cool your cable network is.

Ecommerce entrepreneurs may also face these regulations, depending on the type of product they sell. Pharmaceuticals are, for good reasons, heavily regulated products that not just anyone can manufacture and sell online. Patents are another thing that can prevent competitors from entering a market, as they stop others from copying or using someone else’s proprietary technology. There can be ways to work around these patents, but it can significantly slow down new entrants.

Another example of a barrier to entry is the high upfront capital required to enter some industries. Anyone can start making candles to sell on Etsy: the required investment in terms of cash, equipment, and knowledge is minimal. Mass-producing cars is another story, as it requires huge amounts of resources.

Barriers to entry can be created by the current competitors (for example, if the existing companies make their product or service so technical that it requires tons of assets to even get started and register several patents). In some cases, large companies can influence regulators (for example, through lobbyists) and get them to restrict entry to some markets.

Barriers to Profitability

Barriers to profitability do not prevent a company from entering a market but can make it very difficult to operate profitably. If a company manages to go through the barriers to entry, it can technically launch its product or service. But it won’t have a chance to gain significant market share until it can also pass the barriers to profitability.

In the early days of coffee pods, Nespresso launched its espresso machine and pods. For a long time, Nespresso made sure only their pods could be used with the Nespresso machine, and customers wanting to try another brand of pods had to get a different machine that was compatible. Some companies were able to work around technical and legal restrictions to come up with their own machine and pods. However, the high switching cost for the customers who already had an Nespresso machine made it difficult for new entrants to capture a large share of the market. It took many years for companies to successfully compete with Nespresso. Some of them found an interesting angle: they did not focus on the espresso market but offered a wider variety of hot beverages.

There are many other types of barriers to profitability that can seriously slow down new entrants. Brand loyalty makes customers less likely to buy from a new company (I have my favorite ice cream brand ; I wish other companies good luck trying to get me to buy their brand!).

Network effects make a product more valuable when many people already use it. For example, a social network or an online video game is more fun when all your friends are already using it. Launching a new dating app isn’t technically difficult, and many people tried. But would you sign up if there were a dozen users in your city?

In many cases, pricing is very important to customers, and it can be tempting for new entrants to compete on price. However, competing with existing low-cost companies can be difficult, as the leaders most likely benefit from economies of scale, an innovative business model, and/or their expertise. It isn’t impossible, and new entrants disrupt established industries all the time, but that is not an easy task.

Barriers to profitability can be created by existing competitors, who want to maximize their profits and market share while making it as difficult as possible for new entrants to compete. They will design their product in a way that makes it difficult to copy, will do their best to keep their customers as loyal as possible, restrict access to distribution channels, or slash prices to drive new entrants out.

Conclusion

All these barriers to entry restrict the feasibility of a new business venture, but the potential for success should be considered when working on a business plan. Just because an entrepreneur can enter a new market does not mean they have the ability to be successful. Existing competitors will do their best to make it as difficult as possible. That is one of the reasons that make me believe entrepreneurs should have a strong, unique value proposition that does not put them in the exact same competitive space as other companies.